As The NFL Negotiates a New Partner for NFL Sunday Ticket, Amazon Appears To Be In The Lead

Last week, I talked to various individuals tied to the current negotiations between the NFL and CBS, NBC, ESPN and FOX as it pertains to broadcast TV and streaming rights for NFL content. Currently, FOX has the NFC conference rights and AFC conference rights are with CBS. NBC has “Sunday Night Football”, ESPN has “Monday Night Football” and FOX and the NFL Network have “Thursday Night Football”. ESPN’s deal with the NFL expires after the 2021 football season and all the other broadcast deals run through the 2022 season.

While there’s a lot of speculation on which broadcasters might get more or fewer games in the new deals for broadcast TV rights, (“rumored” to be valued at $100B across all networks for 8-10 years), I’m more interested in what the NFL will end up doing with the “NFL Sunday Ticket” package. It’s well known that the current NFL deal with DIRECTV (AT&T), which runs through the 2022 season, will not be renewed. This makes sense since AT&T is trying to sell off the DIRECTV business and I’m told the NFL no longer wants the restrictions that come from distributing the package via satellite, which is completely outdated, as is the current streaming experience.

DIRECTV extended their current contract with the NFL in 2014 and as we all know, seven years later, the business models for the packaging and distribution of video content has drastically changed. This leaves a new platform to become the NFL’s partner on selling a streaming package to consumers, without any legacy restrictions. Multiple people I spoke with said that while talks are still in the early stages, Amazon looks to be in the lead for the new digital direct-to-consumer offering of what is currently branded NFL Sunday Ticket.

In 2020, Amazon signed a three-year agreement with the NFL to keep Amazon as the exclusive partner for live streaming Thursday Night Football games, 11 in total, and Amazon streamed an exclusive national regular-season game December 26, on Prime Video and Twitch. Sources tell me the NFL has been very happy with Amazon’s live streaming production of the 2020 NFL season, so it would be a natural fit for the NFL to extend their relationship with Amazon on a NFL-based streaming subscription product.

Of all the companies you would think of for such an offering, Amazon would make the most sense for the NFL since Amazon can put their marketing power behind it, already has subscriber’s payment info on file and has the resources to execute what would be a very complex video workflow on the backend. Prime Video and Twitch coverage of the NFL is already available to more than 150 million paid Prime members worldwide, and is in more than 240 countries and territories, so Amazon would give the NFL the widest distribution. I can easily imagine Amazon boxes showing up at my house printed with NFL Sunday Ticket promotions like we’ve seen Amazon do with content partners in the past (Minion boxes everywhere!).

Some have suggested Google, Facebook or even Disney, with their ESPN+ offering might be interested in the deal, but Disney would not take it on, nor are they setup to handle it. Even for broadcast TV rights, Disney is being cautious. On Disney’s Q4 2020 earnings call they were asked about the NFL renewal and said, “first priority will be to look and say does it make sense for shareholder value going forward?” Disney still has a lot of work ahead growing and maintaining their own D2C offerings, so building out an entirely new D2C product with the NFL simply isn’t doable for them from a technical stack standpoint.

With respect to Google, Facebook and Apple, I don’t see the NFL Sunday Ticket fitting into any of Google’s current offerings and it would not make sense to try and bundle it in with any kind of YouTube TV or YouTube Music package. I’ve seen some suggest that bundling an NFL offering with YouTube TV would give Google a way to sign up more subs for their vMVPD service, but many wouldn’t be interested in the vMVPD offering and the additional cost. YouTube TV costs $65 a month now and YouTube just announced more “add on” features coming to YouTube TV for an additional unknown cost.

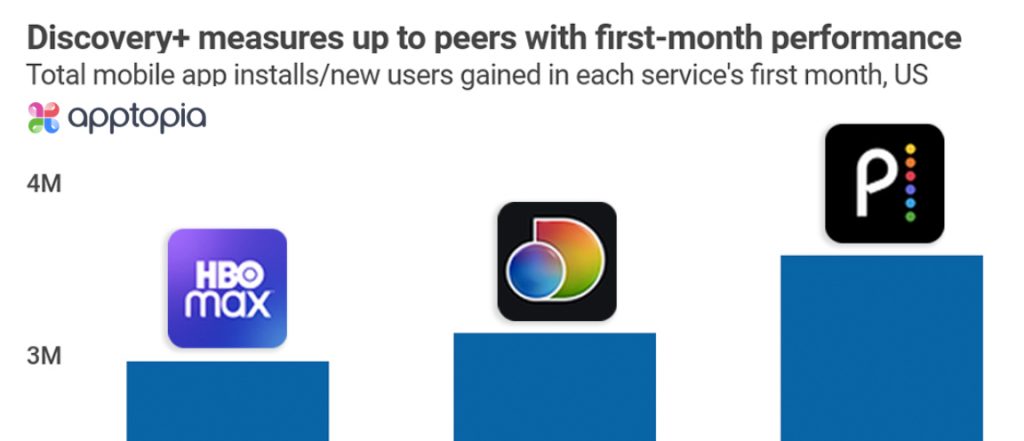

As far as reach goes, the last number Google has publicly given out on subscribers is that YouTube TV has 3 million paying members, a figure they gave out in October of last year and didn’t update during their earnings call in February 2021. YouTube TV launched 4 years ago this month and in that time hasn’t gotten much traction for the service. They look similar to Hulu, which ended 2020 with 4 million paying subs for their Hulu + Live TV offering, losing 100,000 subs year-over-year. The price of live services have all seen very steady increases and not gotten the number of subscribers many thought they would. We saw estimates from analysts and Wall Street firms suggesting Google would get 10 millions subs or more, for the then priced $35 YouTube TV service, within the first year of launch. One could suggest that YouTube could sell a lot of ads against the NFL’s content and share that revenue with the NFL, but that’s something Amazon could do as well. Amazon’s ‘Ads and other’ business did $21.5B of revenue in 2020.

Facebook and the NFL did a content agreement in 2017 which was renewed in 2019 and expired at the end of 2020. As part of the old deal, Facebook didn’t have any live games and provided game recaps that it placed on its Facebook Watch video-on-demand platform. Facebook had to pay an up-front fee for the content and then also split ad revenue with the NFL. In 2016, Facebook did show interest in acquiring rights for live streaming the Thursday Night Games that Amazon ended up getting, but five years later one has to wonder if live streaming of NFL games fits into Facebook’s content road map anymore. When it comes to Apple you have to throw them into the mix due to their reach, but to date Apple hasn’t done anything on the live side, or at scale with video. I know some will suggest they have a younger demographic the NFL wants and the ability to promote services through all the Apple devices and their ecosystem, but I’m not convinced it fits their content strategy.

Based on everything I hear from those closer to these deals than I am, Amazon is in the driver’s seat for the NFL’s new direct-to-consumer offering, although negotiations are early and still ongoing. I’m told that details around pricing for a new streaming NFL Sunday Ticket package and revenue splits have yet to be discussed and that discussions will move along once the NFL finishes the renewals with TV broadcasters. Whomever gets the NFL Sunday Ticket deal, the new streaming service is going to be an exciting product for consumers and will be a huge improvement on what is currently an outdated user experience. And if working with Amazon enables the NFL to bring the price down on a streaming service, which is what Amazon does with all products, the NFL would get a bigger audience, wider distribution for their brand and more revenue based on volume. My bet is on Amazon.

Between all the craziness on Wall Street and the number of earnings in the past few days, it’s been a busy week to say the least. With earnings from NBCU, AT&T, Verizon, Facebook, Apple, Microsoft and Charter, along with news from Sling TV, Peacock, YouTube and others, there’s a lot that’s taken place. I’ve broken down all the earnings, news and concise takeaways at the links below to try and make it easy for everyone to catch up on what they may have missed:

Between all the craziness on Wall Street and the number of earnings in the past few days, it’s been a busy week to say the least. With earnings from NBCU, AT&T, Verizon, Facebook, Apple, Microsoft and Charter, along with news from Sling TV, Peacock, YouTube and others, there’s a lot that’s taken place. I’ve broken down all the earnings, news and concise takeaways at the links below to try and make it easy for everyone to catch up on what they may have missed: