[The short URL for this blog post is cdnmarket.com] You can download this post as a PDF here. The market for third-party CDN services, which I define as the delivery of video and both small and large objects, was about $5 billion in 2023. This figure does not include revenue for services tied to security (WAF, DDoS, etc.), compute, hardware, and storage and excludes delivery in China. The number excludes any company with its own DIY CDN, like Netflix and YouTube, that doesn’t sell its infrastructure as a service to other companies. UPDATED: June 30, 2025: Special CDN Podcast: The Latest on Delivery Pricing, Capacity Planning, DIY, Latency and Bitrate Trends]

The figure also excludes revenue from vendors that offer online video platforms, including Brightcove, Uplynk, AWS Media Services, Quickplay, Deltatre, Mediakind, Sports Radar, Cognizant, Endeavor Streaming, StreamAMG, and Bedrock Streaming, which collectively generated approximately $1.8 billion in revenue in 2023. Based on my knowledge, AWS Media Services is the largest of the group, with roughly $450 million in revenue in 2023.

While reports from research firms claim the CDN market is multiple times larger than my estimate, they are incorrect. Full stop. Do not buy their reports. Akamai, Fastly, Edgio, CDN77, and others disclose sufficient details about their delivery revenue, providing a solid foundation for market sizing. The market is not as large as many suggest, and those writing about the size of the CDN space often fail to define it, including non-CDN services such as transcoding, hardware, hosting, storage, and transit in their numbers.

In most cases, these reports also include vendors who no longer exist in the market. Limelight Networks is frequently mentioned, yet it changed its name two years ago. CenturyLink changed its name to Lumen four years ago, and MaxCDN was acquired eight years ago. These bad reports also list the vendors AT&T and Rackspace, neither of which has its own CDN but instead resells Akamai and other third-party services. Reports also list vendors like Imperva and Fortinet that don’t sell CDN services but cloud security services.

Many incorrectly use public revenue numbers from Akamai and others, redefining revenue as video when that’s not how the companies report it. Akamai breaks out company revenue into three buckets: “Delivery,” “Security,” and “Compute.” Fastly uses the terms “Network Services” (solutions designed to improve the performance of websites, apps, APIs, and digital media), “Security” (products designed to protect websites, apps, APIs, and users) and “other” (emerging products offering which includes compute and observability products). It’s essential to understand these distinctions to accurately interpret the revenue figures.

Limelight Networks previously defined its revenue as “delivery” because that was its primary service at the time. In their SEC filings, they reported that nearly 80% of their revenue was tied to “delivery” services. Since Edgio’s acquisition of Layer0 and Edgecast, its revenue is now blended across services beyond just bit delivery. With Edgio’s subsequent filing, we must see how they bucket and define their revenue. However, we know the revenue Layer0 and Edgecast generated when acquired, separate from the Uplynk business. CDN77 breaks out revenue with the definition of “content delivery,” but no vendor has ever broken out revenue explicitly tied to the delivery of video content. Only once did Akamai disclose, during its 2021 investor summit, that for fiscal year 2020, 57% of all bits it delivered under the “Edge Delivery Traffic” heading were OTT/video. We all know that delivering video accounts for the largest share of bits on any CDN while contributing the least profitability as a service.

There are three main reasons the CDN market has not grown at a higher CAGR over the past few years and is expected to remain in the low single digits going forward. The first reason is that since the pandemic, companies have strived to be more efficient and do more with less. More than two years ago, I documented how many streaming services focused on optimizing their bitrates and, in some cases, reduced the highest rungs from their bitrate ladders to save money. Content owners, including Disney+ Hotstar and the BCC, documented on their tech blogs how they reduced the number of bits they delivered and optimized other cloud-related services to save money.

During Akamai’s Q2 2022 earnings call, the company highlighted this trend among customers and noted a reduction in video bits delivered due to bitrate optimization. What began as a trend during the pandemic has now become the new norm. An interesting data point that recently came to light in Paramount Global’s presentation discussing their plans after the merger with Skydance is the company’s goal to “Unify cloud providers for all distribution services (e.g., Paramount+, Pluto) to provide CDN efficiencies.” Cost savings are the priority.

Previously, many clients evaluated traffic metrics, usually every quarter and allocated traffic at the regional level. Now, evaluations happen within days for some accounts or almost in real time for others, with traffic routing within a multi-CDN stack becoming significantly more dynamic and occurring at the country or even single-ISP level. As a result, more customers are no longer willing to make year-long and high-volume commitments. A data point supporting this comes from Fastly’s Q1 2024 earnings call, where the company stated, “We are seeing a slight uptick on the typical level of rerates with our largest customers, but we have not yet seen the commencement or a traffic expansion usually associated with this motion.” In other words, there is pressure on CDN pricing, as always, with the largest customers demanding lower pricing, even without offering more traffic or larger commitments.

The second main reason for CDN vendors’ lack of revenue growth is that a small number of customers account for a disproportionately large share of revenue. By my estimate, fewer than 50 CDN customers account for 75% of revenue generated by third-party CDNs. We have data to back this up. For example, as of December 31, 2020, Limelight’s top 20 customers accounted for approximately 75% of their total revenue. Notably, two customers, Amazon and Sony, accounted for approximately 36% and 11% of their total revenue, respectively. Akamai had not broken out its customer split the same way, but for many years, it disclosed that when it broke out revenue under the “media” bucket, six customers accounted for 18% of its media revenue at the high point.

In Q1 2024, Akamai’s delivery revenue declined 11% year-over-year due to lower bitrates and pricing among a small concentration of large customers. Many assumed the decline was due to Akamai losing market share, but that wasn’t the case. Lower bits, combined with lower pricing, equal a shrinking market for all CDN vendors. Multiple large customers repricing in the same quarter or year hurt revenue growth. I’ll publish a post shortly on CDN pricing and the highlights from my latest survey.

So, who are the largest CDN customers? Here’s a list of customers spending more than $100 million annually on delivery services. It includes companies that use third-party CDNs to deliver video, software downloads, and small objects, but it is not exhaustive. Many customers are making revenue commitments with CDNs across all services offered, so contracts from the largest customers vary widely, with many variables depending on the type of traffic and regions.

The list consists of Amazon Prime Video, Disney, Comcast, Paramount Global, Warner Bros. Discovery, TikTok, Microsoft, Apple, Sony Entertainment Network, Nintendo, Activision Blizzard, Electronic Arts, Riot Games, Valve, Take-Two Interactive, Roblox, Ubisoft, Roku, NFL, MLB, ESL FACEIT Group, Spotify, Reliance Industries (Jio), TV18 (Viacom18), Snap, The Times Group and Reddit amongst others. I’ve been collecting CDN pricing data for almost twenty years, routinely speaking with many of the companies mentioned, and some public data points can be examined and tied to traffic volumes and public filings to obtain numbers. For instance, when Reddit filed to go public, its S-1 stated that it planned to spend at least $385 million on cloud services by September 2026. Many of the details I have from customers about what they buy from CDN vendors are off the record, or I am under an NDA that prohibits me from disclosing them.

The third reason for the challenging market conditions is that 4K streaming is simply not in demand among consumers and isn’t driving increased data usage. Many streaming services charge more for 4K streaming, and consumers have shown that, in most cases, they are not willing to pay the extra cost. And yet, the industry still wants to hype 4K, 8K, VR and AR as if they are catalysts for CDNs, which they aren’t. No NFL game, including the Super Bowl, is in 4K. Neither are streams from the NHL, MLB, MLS, or cricket games on Disney+ Hotstar and JioCinema. In 2014, I wrote a blog post entitled “The Dirty Little Secret About 4K Streaming: Content Owners Can’t Afford The Bandwidth Costs,” which remains true ten years later. Even big companies that can afford the additional costs of 4K, such as Amazon, Google, and Apple, don’t offer 4K for Thursday Night Football, NFL Sunday Ticket, or Friday Night Baseball. In 2022, multiple CDNs informed me that, of all the bits they would deliver that year, 4K/UHD would account for “less than” 10%, with no year-over-year change. Last year, it was flat as well.

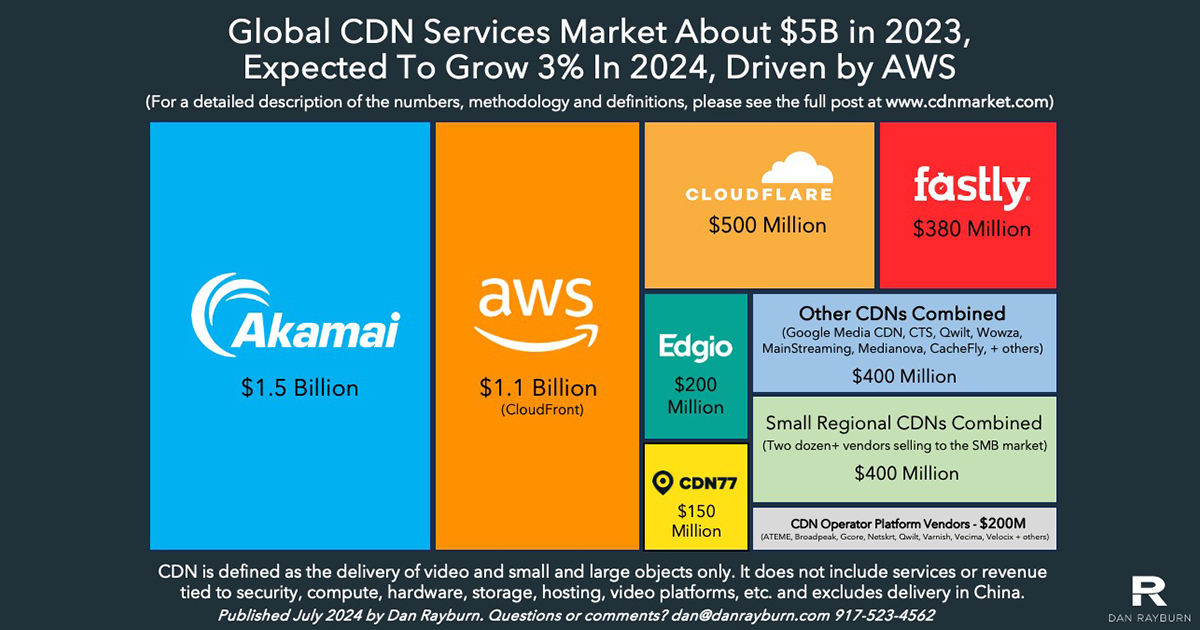

As I stated earlier, the total revenue of all vendors offering delivery services, excluding China, was about $5 billion in 2023. This includes delivery revenue from vendors listed at cdnlist.com, including Akamai, Amazon (CloudFront), CDN77, Cloudflare, Comcast Technology Solutions, Edgio, Fastly, Google Cloud Media CDN, MainStreaming and Qwilt. It also combines revenue from smaller vendors into one number, including Bunny, CacheFly, CDNsun, Gcore, GlobalConnect, KeyCDN, Medianova, and other small regional CDNs.

In 2023, Akamai reported $1.54 billion in delivery revenue, an 8% year-over-year decrease. From 2021 to 2023, Akamai’s delivery revenue declined by over $300 million due to reduced bit delivery, limited adoption of 4K video, lower pricing, and the adoption of a multi-CDN strategy by all large customers. These market trends impact Akamai the most, since it is the largest vendor in delivery revenue. Amazon doesn’t disclose its income from CloudFront, but I estimate it to be $1.1 billion in 2023. I am not disclosing my source for the number, but note that at one point, Amazon published the number of paying customers it had on CloudFront.

Cloudflare reported $1.29 billion in company revenue for 2023, a 33% year-over-year increase, of which I am counting $500 million towards my market sizing numbers. Cloudflare offers many cloud security and DNS services that do not fall under my definition of delivery, and the company does very little in streaming. Fastly had $506 million in total revenue, of which I am counting $380 million towards delivery. Based on Fastly’s guidance for Q1 2024, 79% of their revenue in the quarter came from “Network Services,” which includes delivery. While we await an updated filing from Edgio, the company guided to $392 million at the midpoint in November 2023. Some of that revenue is tied to security and application services, as well as Edgio’s Uplynk platform, so I am using $200 million from their revenue guidance to size the market. CDN77 disclosed that its 2023 revenue was in the $140M–$150 million range and that it expects 40% growth in 2024. According to my projections, the six largest CDNs combined generated $3.8 billion in revenue in 2023, accounting for 74% of the total market.

Outside of the top six most prominent CDN vendors, all other CDNs have less than $100 million in revenue. None of them, including Google, CTS, MainStreaming, Medianova, CacheFly, or Qwilt, discloses revenue numbers publicly, and the numbers I have been given are under NDA or provided to me only on a background basis. Grouping them all would result in another $400 million in 2023 revenue. In addition, many smaller regional CDNs worldwide target SMB customers and low-traffic customers. By my last count, at least two dozen vendors fell into this category, with an estimated $500 million in combined annual revenue. It is worth noting that although all these vendors fall under the delivery revenue category, they don’t all compete. Many smaller customers spend less than $100 monthly, which is not a segment of the market that Akamai, Fastly or Edgio target. Adding up all these numbers yields a total 2023 revenue of $4.7 billion.

In addition to the revenue from CDN services, approximately $200 million was generated in 2023 from vendors offering CDN platforms to operators and carriers. These vendors include ATEME, Broadpeak, Gcore, Jet-Stream, Netskrt, Qwilt, Varnish Software, Vecima, and Velocix, which license their software/platform to carriers, network operators, and content owners who have a DIY CDN as part of their overall delivery strategy. While some of the vendors mentioned, such as Broadpeak and ATEME, are public, none of the vendors break out the percentage of their revenue tied directly to their CDN platform offerings. My $170 million figure discounts their total revenue by the percentage I believe is allocated to their CDN product. Additionally, in many cases, the vendor has privately informed me of the revenue rate without allowing me to break it down by vendor. The market for selling CDN platforms to carriers, network operators and content owners is tiny. In 2023, Broadpeak’s overall revenue was down 6.8% year-over-year.

Combining all vendors in the market, broken out by content delivery as I define it, puts the market’s 2023 revenue at $4.9 billion. That number could fluctuate by a few hundred million, depending on how much of a company’s total income is allocated to “delivery.” However, as you can see, the numbers reported by firms claiming the CDN market was $25.5 billion, $21.3 billion, $16.3 billion, or $13.2 billion are all incorrect. Do not use those numbers. Overinflating the market’s size helps no one and sets false expectations.

Given Amazon CloudFront’s offerings, I anticipate the CDN market will grow in 2024. While most other large CDNs, including Akamai, Edgio, and Fastly, are experiencing year-over-year revenue declines, I expect Amazon’s CloudFront revenue to grow by 10% or more this year. Cloudflare and CDN77 are also likely to see growth in their delivery business, which will help offset revenue declines from other CDN vendors and contribute to the overall market’s approximately 3% growth in 2024. Without Amazon and Cloudflare growing, the CDN market’s revenue growth would have been negative in 2023 and 2024. Amazon is capturing a larger share of traffic in specific regions, including for cricket events in India and other major live events, as recently demonstrated by Peacock’s NFL Wild Card game. All customers of Peacock’s size use multiple CDNs, but they adjust how they allocate traffic distribution. I’ve seen Amazon capture a larger share of traffic for large-scale live events, and I expect that trend to continue.

If you have any comments or questions on the topic, you can put them in the comments section on this post on LinkedIn or contact me directly at dan@danrayburn.com

Listen to my special CDN-focused podcast from July 2024 for more details and updates regarding 4K, low/ultra-low latency, CMCD, DIY (TikTok, Disney), Open Caching, pricing and multi-CDN.

Note: I have never bought, sold, or traded shares in any public CDN, and even in my managed portfolios, Akamai, Fastly, Cloudflare, and Edgio are excluded.